Updated May 2026

What Is Bodily Injury Liability Insurance?

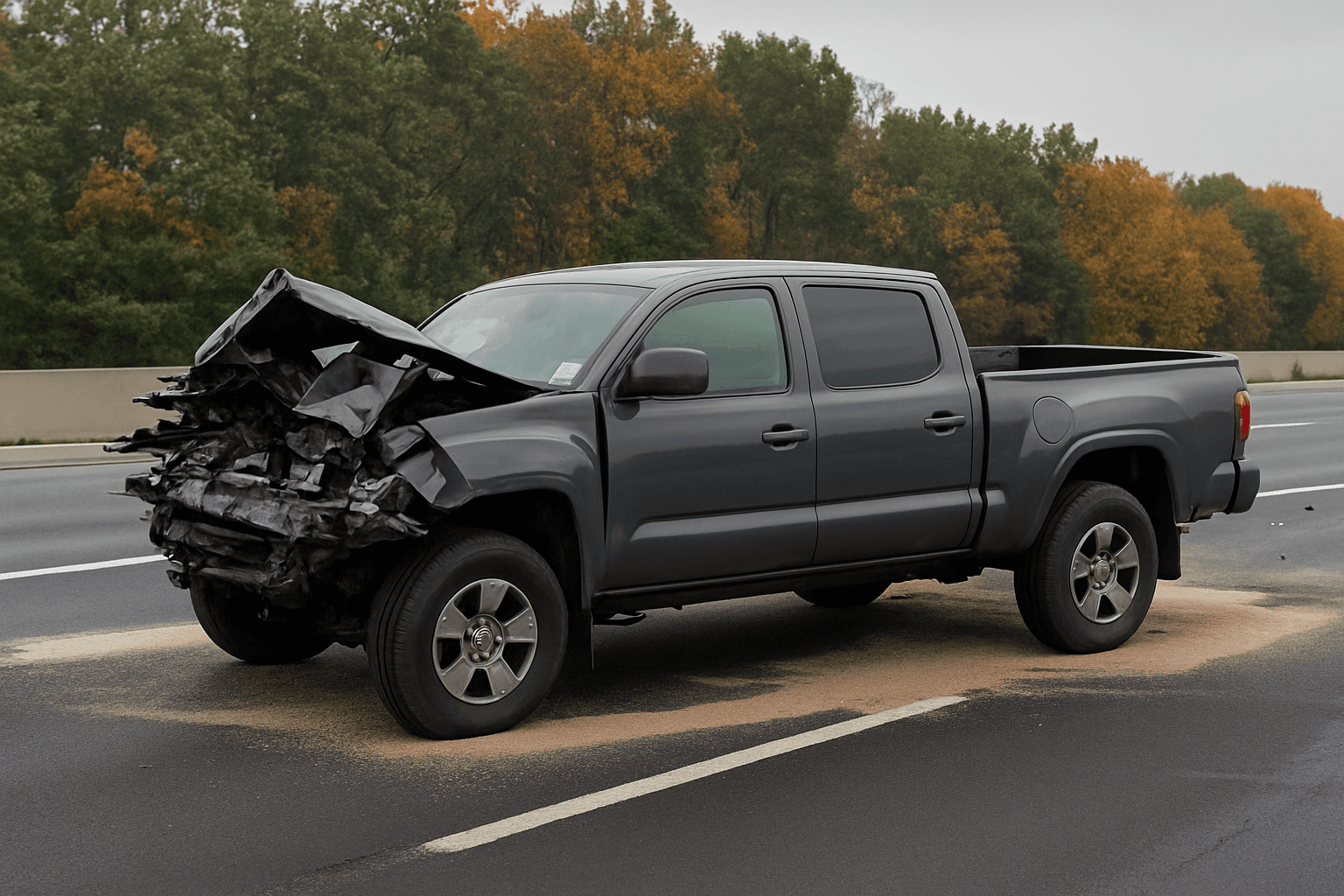

Bodily injury liability pays medical expenses, rehabilitation costs, lost income, pain and suffering damages, and legal defense fees when you injure someone in an at-fault accident. Coverage is expressed as split limits: the first number caps what the insurer pays per injured person, the second caps total payout per accident. If you cause an accident with injuries exceeding your limits, you pay the difference out of pocket—creditors can pursue your wages, bank accounts, and property.

- You rear-end a sedan at a red light. The driver has $18,000 in medical bills and $6,000 in lost wages. The passenger has $9,000 in medical costs. You carry 25/50 limits. Your insurer pays $24,000 to the driver (capped at your $25,000 per-person limit) and $9,000 to the passenger, totaling $33,000. You owe the driver the remaining $0 because the per-person cap applied first, but if a third person were injured and the total exceeded $50,000, you'd pay the overage yourself.

- You run a stop sign and T-bone another car. The driver suffers a broken pelvis and requires surgery—total medical costs reach $87,000, plus $22,000 in lost wages and $15,000 in pain and suffering. Your 50/100 limits pay the full $50,000 per-person maximum. The injured driver's attorney files a judgment against you for the remaining $74,000. Creditors garnish your paycheck and place liens on your home.

- You missed court for an uninsured-driving ticket. After clearing the FTA and paying the original fine, your state requires SR-22 filing and proof of bodily injury liability before reinstatement. You purchase 25/50 coverage through a non-standard carrier at $110/month. The SR-22 itself costs $25 to file. Without this coverage, the DMV won't lift the suspension—even though the FTA hold is cleared.

How Much Does Bodily Injury Liability Insurance Cost?

Bodily injury liability typically adds $40–$90 per month to your premium, or $480–$1,080 annually, depending on your state's minimum requirements and your coverage limits.

- State-mandated minimums: California requires 15/30, Alabama requires 25/50, and Alaska requires 50/100, directly affecting base cost.

- Driving record: An at-fault accident in the past three years raises bodily injury premiums 30–60% because insurers expect higher claim risk.

- Coverage limits chosen: Increasing from 25/50 to 100/300 limits typically adds $15–$35 per month but protects assets above state minimums.

- Suspension history: Drivers reinstating after an FTA hold pay 20–50% more for the first policy term due to lapse in continuous coverage.

- Age and experience: Drivers under 25 or with fewer than three years of licensed driving history pay 40–80% more due to higher accident rates.

- ZIP code claim density: Urban areas with higher pedestrian traffic and accident frequency increase bodily injury costs 10–25%.

See How Much You Could Save

Get personalized bodily injury liability insurance quotes in minutes.

Who Needs Bodily Injury Liability Insurance?

You need bodily injury liability if you're reinstating after an FTA hold and the underlying citation was uninsured-driving, reckless driving, or another violation requiring SR-22—your state won't lift the suspension without proof of coverage. You also need it if you own assets a lawsuit could reach: a home with equity, a retirement account, or wages above garnishment-exempt thresholds. State minimums are legally sufficient but financially inadequate if you cause serious injuries.

Calculate your asset exposure: add home equity, savings, retirement accounts, and annual income. If that total exceeds $50,000, carry at least 100/300 limits. If you're reinstating after FTA and SR-22 is required, you have no choice—you must carry at least state minimums to restore driving privileges. If your underlying citation didn't require SR-22 and you have minimal assets, state minimums satisfy legal requirements but won't protect you in a severe accident.