Updated May 2026

What Is Property Damage Liability Insurance?

Property damage liability pays for damage your vehicle causes to someone else's car, fence, building, or other property when you're at fault in an accident. It does not cover your own vehicle or property. Every state sets a minimum coverage amount—typically between $5,000 and $25,000—and you cannot legally drive without at least that minimum. If your FTA suspension stemmed from an uninsured-driving citation, proof of property damage liability coverage is often required before the DMV will lift the hold, even after you've cleared the bench warrant and resolved the underlying ticket.

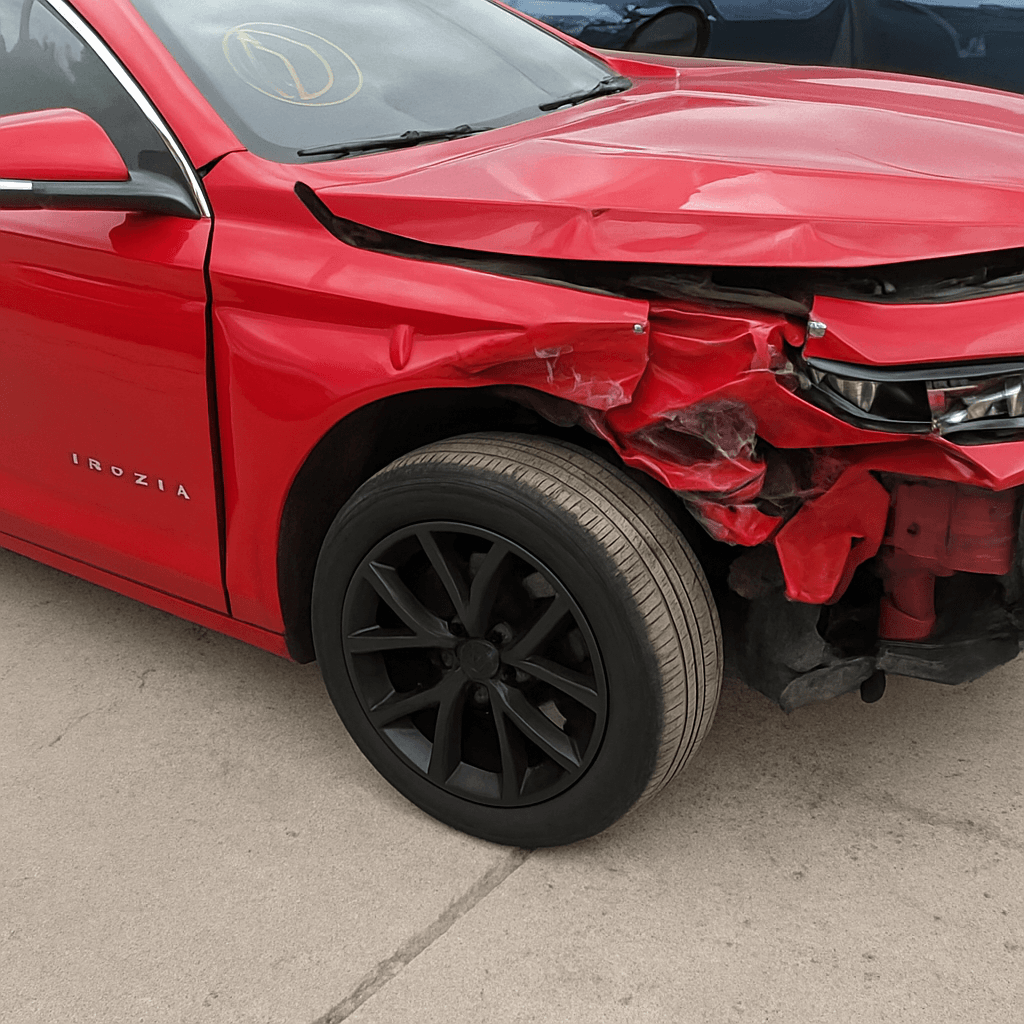

- You're distracted at a stoplight and rear-end the car ahead of you, crushing their rear bumper and trunk. Repair estimate is $6,800. Your property damage liability coverage pays the $6,800 directly to the other driver's repair shop or insurer. If you carry only your state's $5,000 minimum, you owe the remaining $1,800 out of pocket—and the other driver can sue you for it.

- You lose control on ice and slide into a parked car in a grocery store lot, causing $4,200 in damage to the other vehicle. Your property damage liability pays the full $4,200. The parked car's owner never files a claim on their own policy, because your liability coverage handled it. No deductible applies to liability coverage—the full covered amount is paid by your insurer up to your policy limit.

- You misjudge a turn and crash through a homeowner's wooden fence, destroying 40 feet of fencing valued at $3,600. Property damage liability covers the fence repair. If you also damaged your own vehicle, that's a separate collision claim on your own policy—property damage liability only addresses the fence, not your car.

How Much Does Property Damage Liability Insurance Cost?

Property damage liability adds approximately $15–$35 per month ($180–$420 annually) to your premium for state minimum limits. Higher limits—$50,000 or $100,000—add $25–$50 per month.

- Coverage limit selected: $10,000 minimum costs less than $50,000, but leaves you exposed if damage exceeds the limit.

- Driving record: prior at-fault accidents or property damage claims increase your rate significantly, often 20–40 percent above clean-record pricing.

- Zip code: urban areas with high accident density and higher vehicle values push property damage rates up compared to rural areas.

- Vehicle type: insuring a heavy truck or SUV costs more because those vehicles tend to cause more expensive property damage in collisions.

- Bundling: combining property damage liability with collision and comprehensive often reduces the per-coverage cost through multi-coverage discounts.

- FTA status: some carriers treat an FTA suspension—especially if the underlying citation was uninsured driving—as a high-risk signal and price property damage liability 15–30 percent higher until you maintain continuous coverage for 6–12 months.

See How Much You Could Save

Get personalized property damage liability insurance quotes in minutes.

Who Needs Property Damage Liability Insurance?

You need property damage liability if you're reinstating a license after an FTA suspension tied to an uninsured-driving citation, or if your state requires proof of coverage before lifting the hold. Even if the FTA was for a completely unrelated citation—speeding, parking, failure to yield—you still cannot drive legally without at least your state's minimum liability coverage, which includes property damage. If you were driving uninsured when you missed court, expect SR-22 filing on top of the coverage itself.

If your FTA suspension is cleared and the underlying citation did not involve uninsured driving, purchase your state's minimum property damage liability to satisfy reinstatement requirements. If the citation was for driving uninsured, or if you caused an accident while uninsured, expect to file SR-22 and carry higher limits—often $25,000 or $50,000—for three years as a condition of reinstatement. Carriers will not quote you until the bench warrant is recalled and the court releases the FTA hold to the DMV.